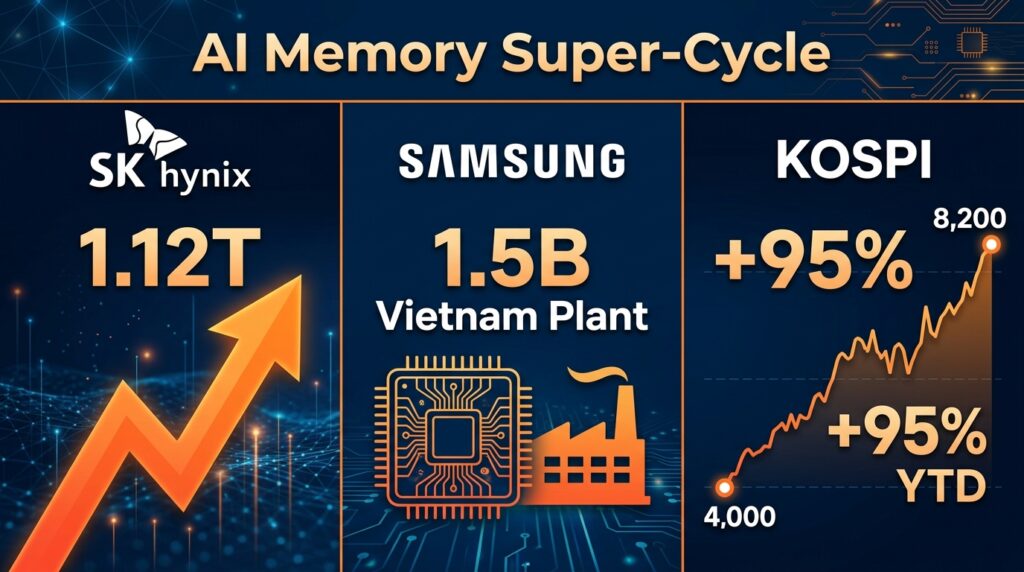

The South Korean memory chip industry has reached a new milestone. On May 27, 2026, SK Hynix surpassed the 1 trillion won market value threshold, closing the session at 9.31 trillion won; Samsung Electronics joined the $1 trillion club on May 6, and US-based Micron did so on May 26. Samsung and SK Hynix now collectively account for more than 40% of the benchmark KOSPI index, which has surged 95% in 2026 after rising 76% last year. This is not a temporary market spike. According to SK Hynix, memory chip demand will continue to exceed supply through 2028, keeping price levels elevated.

This article explains why the memory industry is in a structural “super‑cycle,” how AI is transforming memory from a commodity into a specialized growth engine, and what Samsung’s new Vietnam plant reveals about the hidden bottlenecks in the AI supply chain.

From Boom‑Bust to Moonshot – How AI Broke the Memory Cycle

For decades, the memory chip industry followed a predictable boom‑and‑bust cycle. When demand rose, manufacturers rushed to build new fabs. By the time those fabs came online, supply would overshoot, prices would collapse, and the cycle would start again.

AI has broken that cycle.

The key change is demand stability. Instead of volatile consumer electronics demand, AI data centers need memory around the clock, 365 days a year. That demand shows no signs of slowing. Counterpoint Research projects that global HBM bit demand for AI server compute ASICs will balloon 35× from 2024 to 2028. AI servers are expected to account for 50–55% of total DRAM demand by 2028, up from just 24% in 2025.

The memory market is projected to reach $551.6 billion in 2026, which is more than double the wafer foundry sector’s projection of $218.7 billion for the same year. Memory’s share of overall semiconductor revenue has climbed to nearly 48% in 2026, a level that industry analysts now describe as a “structural supercycle,” with the cycle projected to sustain beyond 2028.

Perhaps the most dramatic sign of the new pricing power is that memory chip prices doubled in the first quarter of 2026 alone and are forecast to increase by up to 63% in the current quarter. The bottleneck has moved from computing speed to memory bandwidth, with HBM capacity effectively sold out through 2026.

From Commodity to Crown Jewel – The HBM Revolution

The shift is being powered by HBM—high‑bandwidth memory, a specialized stack of DRAM chips that sits directly beside an AI accelerator. Standard memory is a commodity; HBM is a high‑margin, capacity‑constrained product that only a few companies can make. According to Counterpoint Research, SK Hynix will account for 54% of the global HBM4 market in 2026, followed by Samsung Electronics with 28% and Micron with 18%.

SK Hynix’s commanding HBM position has been the primary driver of its ascent. The company’s entire 2026 HBM supply has been fully committed for months, and it is aggressively expanding capacity to keep pace with Nvidia’s product cadence.

After a period of catching up, Samsung has now become the overall leader in the DRAM market, holding a 38% share in the first quarter. It is also regaining HBM momentum. In the first quarter, Samsung held 28% of the HBM market and has reportedly secured Nvidia’s qualification for next‑generation HBM4.

Strong AI data center demand has also lifted the entire memory market. Conventional DRAM contract prices rose 55–60% quarter‑on‑quarter in early 2026, while NAND Flash contract prices increased 33–38% over the same period.

The Trickle‑Up Effect – Legacy Chips and the Collateral Damage

The same AI demand that is enriching memory makers is also creating collateral damage. To meet surging demand for high-margin HBM and advanced DRAM, the major producers are reallocating production capacity away from “legacy chips”—the standard NAND and DRAM used in smartphones, laptops, and automobiles.

This reallocation is the logic behind Samsung’s $1.5 billion chip testing plant in Vietnam. The facility, which will begin operations in November 2027, will focus specifically on testing legacy chips. It is expected to produce an annual capacity of 153.3 billion gigabits of DRAM and 255.6 billion gigabits of NAND.

Samsung intends to reinvest future profits from the project, up to about $2.5 billion, for a potential second factory. This long‑term commitment underscores the industry’s belief that the memory shortage is not temporary. Supplies of both NAND and legacy DRAM are expected to remain tight through 2028.

Vietnam is also becoming a strategic beneficiary of the AI hardware shift. Samsung is already Vietnam’s largest foreign investor, having committed over $23 billion. Domestic Vietnamese companies FPT and Viettel are building the country’s first 32nm semiconductor fabrication facility, targeting pilot production for 2028. The country’s growing semiconductor footprint is being driven by “China+1” supply chain diversification, as companies look to reduce their reliance on China.

The South Korea Effect – A Nation’s Economy Rides on AI Memory

The memory supercycle is not just a corporate phenomenon. It is a national one. South Korea’s KOSPI index rose as much as 5.1% on 27 May, hitting an all‑time high of 8,457 and triggering a “sidecar” curb that temporarily halted algorithmic trading.

The index has nearly doubled since the start of the year, a performance on track to rival the Nasdaq 100’s 102% surge in 1999 before the dot‑com bubble burst. JP Morgan has noted that the current rally is primarily driven by Korea’s unique position as a liquid AI hardware proxy outside the US and Taiwan. Samsung and SK Hynix now account for more than 40% of the index’s market capitalization.

South Korea has become the first country other than the United States to have more than one company reach 1 trillion in market value, with Samsung and SK Hynix now joined by TSMC as the only three non-US firms in the 1 trillion club. The country’s economic growth is now tightly coupled to the ups and downs of global AI infrastructure spending, a level of exposure that is both an extraordinary opportunity and a significant source of vulnerability.

Frequently Asked Questions (FAQ)

Q1: What is a “memory supercycle”?

A: In the past, memory demand was tied to volatile consumer electronics. Now, AI data centers need memory around the clock, providing a stable and rapidly growing source of demand. This structural shift, combined with tight supply, has broken the old boom‑bust cycle.

Q2: What is HBM, and why does it matter?

A: High‑Bandwidth Memory is a specialized stack of DRAM chips that sits directly beside an AI accelerator like Nvidia’s GPU. It provides the massive memory bandwidth that AI models require. Only a few companies can make it, and capacity is sold out for years.

Q3: Why are legacy chips in short supply?

A: Major producers are prioritizing high-margin HBM and advanced DRAM for AI data centers. This reallocation is reducing capacity for the standard memory used in smartphones, laptops, and automobiles.

Q4: Why is South Korea’s stock market surging?

A: The KOSPI index has nearly doubled in 2026, driven almost entirely by Samsung and SK Hynix, which together account for more than 40% of the index. South Korea is the only liquid AI hardware proxy outside the US and Taiwan.

Q5: How long will the memory shortage last?

A: Industry analysts and executives expect supply to remain tight through at least 2028, with memory chip demand continuing to exceed supply.

Q6: Why is Samsung building a chip testing plant in Vietnam?

A: To address the severe shortage of legacy memory chips used in smartphones, laptops, and automobiles. The plant will test and package standard memory chips.

Q7: How does this connect to your earlier coverage of HBM as the “new GPU”?

A: Directly. Our earlier article explained why HBM had become AI’s scarcest component. The SK Hynix trillion‑dollar milestone and the Samsung Vietnam plant are the direct consequences of that scarcity.

Q8: What happens if AI infrastructure spending slows?

A: That is the central risk. If large cloud providers reduce their spending, memory prices could fall, and the supercycle could unwind. However, current industry forecasts predict sustained growth through 2028.

Conclusion—The Memory Super‑Cycle Has Only Just Begun

The memory industry has been transformed. What was once a cyclical, commodity‑driven business is now a structural growth engine at the heart of the AI revolution. SK Hynix’s 1 trillion valuation, Samsung’s 1 trillion valuation, Samsung’s 1.5 billion bet in Vietnam, and the KOSPI’s historic rally are all signals of the same underlying trend: AI needs memory, and the companies that supply it are reaping the rewards.

The supercycle is not a short‑term spike. It is a multi‑year structural shift, driven by demand that shows no signs of slowing and supply constraints that will take years to resolve. The memory makers are no longer just supporting players. They are central to the AI story, and their moment has arrived.

References & Further Reading

- Reuters – “Samsung plans $1.5 billion chip testing plant in Vietnam” (27 May 2026)

- Reuters – “SK Hynix joins $1 trillion club after Samsung, Micron on AI chip boom” (27 May 2026)

- Counterpoint Research – “HBM Demand for AI Server Compute ASICs to Grow 35x by 2028”

- TrendForce – “DRAM Market Bulletin” (27 May 2026)

- Sigmaintell – “AI Servers to Account for Up to 55% of DRAM Demand by 2028”

- BusinessKorea – “Samsung Plans $1.5 Billion Vietnam Chip Test Plant” (27 May 2026)

- CNBC – “SK Hynix hits $1 trillion valuation as AI boom lifts South Korean chip stocks” (27 May 2026)

- JP Morgan – “Kospi rally goes beyond Samsung, SK hynix” (25 May 2026)

- The Investor – “Kospi rally goes beyond Samsung, SK hynix: JP Morgan” (25 May 2026)

Leave a Reply