Last updated: May 8, 2026 | Reading time: 13 minutes

Introduction – The Lone Star State’s AI Revolution

For two decades, Northern Virginia reigned as the undisputed capital of global data center infrastructure. Its proximity to Washington, D.C., dense fiber networks, and business-friendly policies made it the default home for the world’s digital backbone. But the AI boom has rewritten the rules.

Today, the center of gravity is shifting west—to Texas.

Between 2025 and 2026, Texas data center market share surged by an estimated 142%, while Virginia’s share contracted by 35%. With 6.5 gigawatts (GW) of capacity already under construction and projections that the state could overtake Virginia as the world’s largest data center market by 2030, the Lone Star State has emerged as the primary expansion frontier for AI infrastructure.

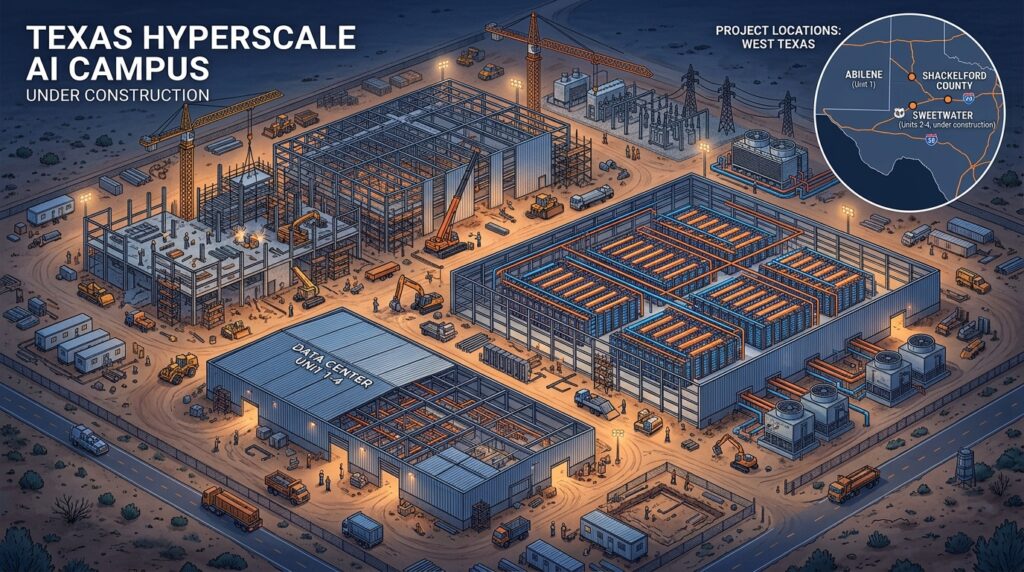

The Stargate campus in Abilene, backed by OpenAI, Oracle, and SoftBank, is rapidly becoming one of the largest AI compute clusters on the planet. Microsoft and Crusoe are building a 900 MW AI factory next door. Vantage Data Centers is pouring $25 billion into a 1.4 GW mega‑campus called Frontier in Shackelford County. And in the most emblematic deal of the era, Nvidia just partnered with IREN to deploy up to 5 GW of DSX‑aligned AI infrastructure, with IREN’s 2 GW Sweetwater campus in Texas as the flagship site.

This article explains why Texas has become the epicenter of the AI build‑out. You will learn the six key drivers behind this geographic shift, the mounting challenges the state faces, and what it means for the future of AI computing.

1. The Power Advantage – Why ERCOT Wins

The single most important factor in choosing a data center location today is power availability. Virginia’s grid, dominated by Dominion Energy, has effectively run out of capacity. Utilities in Northern Virginia have begun imposing moratoriums on new connections, and grid connection timelines now stretch four years or more.

Texas operates under a fundamentally different model. The Electric Reliability Council of Texas (ERCOT) manages a deregulated grid with several unique advantages:

- Abundant “fuel” mix – Texas has more solar, wind, and natural gas generation capacity than any other region in the US. The state added more utility‑scale solar in 2025 than any other.

- Faster interconnection for large loads – Unlike regulated monopoly utilities elsewhere, ERCOT’s market structure allows developers to negotiate directly with transmission providers.

- Behind‑the‑meter power optionality – Several new campuses, including Microsoft and Crusoe’s Abilene facility, are incorporating on‑site power generation directly behind the meter, reducing strain on the public grid.

But success brings scrutiny. In March 2026, the Public Utility Commission of Texas (PUCT) proposed new interconnection standards under Senate Bill 6, requiring large‑load customers (75 MW or greater) to demonstrate project readiness, pay upfront study fees (100,000 to 300,000), and execute intermediate agreements before entering the interconnection queue. These rules aim to prevent speculative projects from clogging the pipeline.

2. Tax Incentives – The $3 Billion Exemption

Texas has aggressively courted data center investment through one of the most generous tax incentive programs in the nation. The state exempts qualifying data centers from paying the 6.25% state sales tax on purchases related to construction and maintenance—hardware, servers, cooling systems, and electrical equipment.

The cost to Texas is staggering. In 2025 alone, the sales tax break amounted to over 1 billion in forgone revenue. The comptroller’s office increased its estimate to over $3 billion for the 2027–2028 biennial budget. The tax break is expected to be worth almost $1.8 billion annually by fiscal year 2030.

Local property tax abatements add another layer. In April 2026, Nolan County approved a 10‑year tax abatement for a 7 billion‑dollar data center project in Sweetwater. A 14.5 billion Cloudburst Data Centers project between Austin and San Antonio secured an estimated $500 million tax abatement and a 10-year development agreement. Milam County granted a 75% abatement over 10 years to a Riot Rockdale facility.

However, the political calculus is shifting. State Senator Joan Huffman, chair of the Senate Finance Committee, has called the growing exemption amounts “extremely concerning” and “unsustainable,” and plans to file legislation to either repeal or significantly limit the tax break. Data center leaders warn that shrinking or ending the incentive could threaten Texas’ rising status as the nation’s number one destination for AI infrastructure.

3. Renewable Energy – Solar and Wind Power the Boom

Texas leads the nation in wind energy production and ranks second in utility‑scale solar. For hyperscalers with aggressive net‑zero commitments, this renewable abundance is a major draw.

In February 2026, Google signed the largest renewable Power Purchase Agreement (PPA) ever in the United States with TotalEnergies: 1 GW of solar capacity to power its Texas data centers over 15 years, delivering an estimated 28 terawatt‑hours of renewable electricity.

Soluna’s 166 MW data center in Willacy County will receive behind‑the‑meter power directly from the Las Majadas Wind Project, curtailing operations under certain market conditions when energy is most needed on the grid.

This renewable capacity serves two purposes: it helps meet corporate climate goals and provides price stability against volatile natural gas markets. The combination of abundant solar, wind, and natural gas gives Texas a fuel‑diverse, resilient grid that can handle the massive, variable loads of AI training clusters.

4. Land, Space, and Construction – The Frontier for Gigawatt‑Scale Campuses

AI data centers are no longer measured in megawatts—they are measured in gigawatts. A single AI factory campus now rivals the output of a nuclear power plant. Texas offers what Virginia and California cannot: vast, flat, undeveloped land with existing transmission access.

The scale of projects underway is staggering:

| Project | Location | Capacity | Investment | Status |

|---|---|---|---|---|

| Stargate (OpenAI/Oracle) | Abilene | 1.2 GW (existing) | ~$47B | Under construction; completion mid‑2026 |

| Microsoft/Crusoe AI Factory | Abilene | 900 MW + on‑site power | Undisclosed | Land clearing underway; switch‑on mid‑2027 |

| Vantage Frontier | Shackelford County | 1.4 GW | $25B | First building operational H2 2026 |

| IREN Sweetwater | Sweetwater (Nolan County) | 2 GW (phase 1: 1.4 GW energized) | Nvidia partnership | Phase 1 energized May 2026 |

Texas leads the nation with 336 planned data center projects, outpacing every other state. Texas alone accounts for 6.5 GW of capacity under construction across more than 400 existing or planned facilities. More than 10 projects of 1 GW or larger are now under construction nationwide—a threshold unimaginable just a few years ago.

The land rush is real, but so are the bottlenecks. Grid connection timelines are lengthening, skilled labor is scarce, and local communities are increasingly vocal about water and infrastructure strains.

5. Water Concerns – The New Environmental Battleground

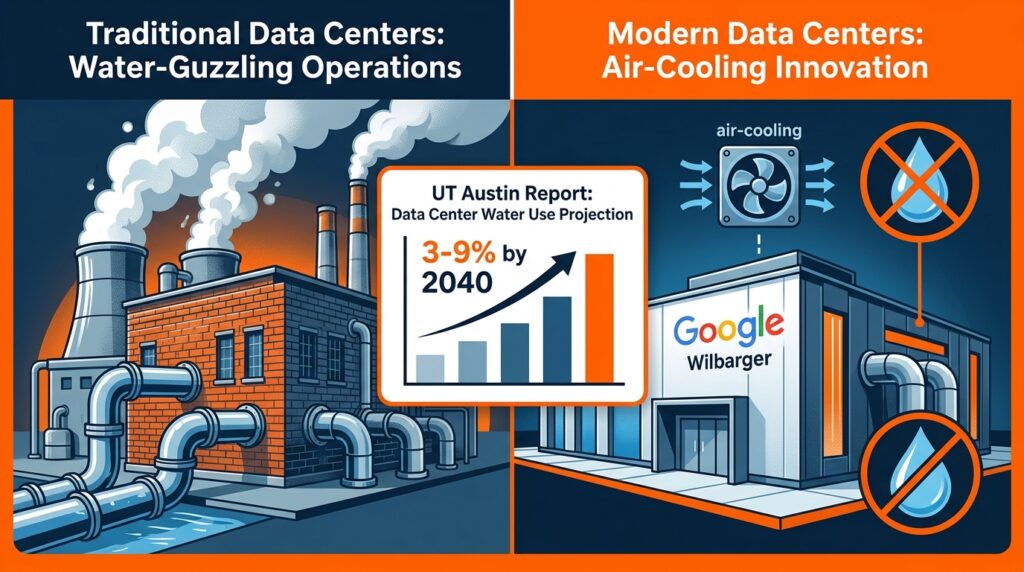

AI factories consume enormous amounts of water for cooling. In a state already facing prolonged drought, groundwater depletion, and a projected $174 billion water supply gap over the next 50 years, water has become the most contentious environmental issue around Texas data centers.

A new report from the University of Texas at Austin estimates that data centers could account for between 3% and 9% of Texas’ total water use by 2040—up from less than 1% today. The Texas Farm Bureau has formally expressed concerns that large data centers may “compete with agricultural production, municipal needs, and long‑term aquifer sustainability”.

In response, developers are aggressively adopting closed‑loop cooling systems. Skybox Datacenters testified to a Texas House committee that its closed‑loop systems use less water than five typical households. The Stargate campus in Abilene, despite its massive scale, consumed only 20 gallons per minute last month—less than 5% of its city allocation.

Google has gone even further. The company’s upcoming data center in Wilbarger County “will use advanced air‑cooling technology, limiting water consumption to only critical campus operations like kitchens”. By eliminating water use for cooling entirely, Google is setting a new standard for arid‑region AI infrastructure.

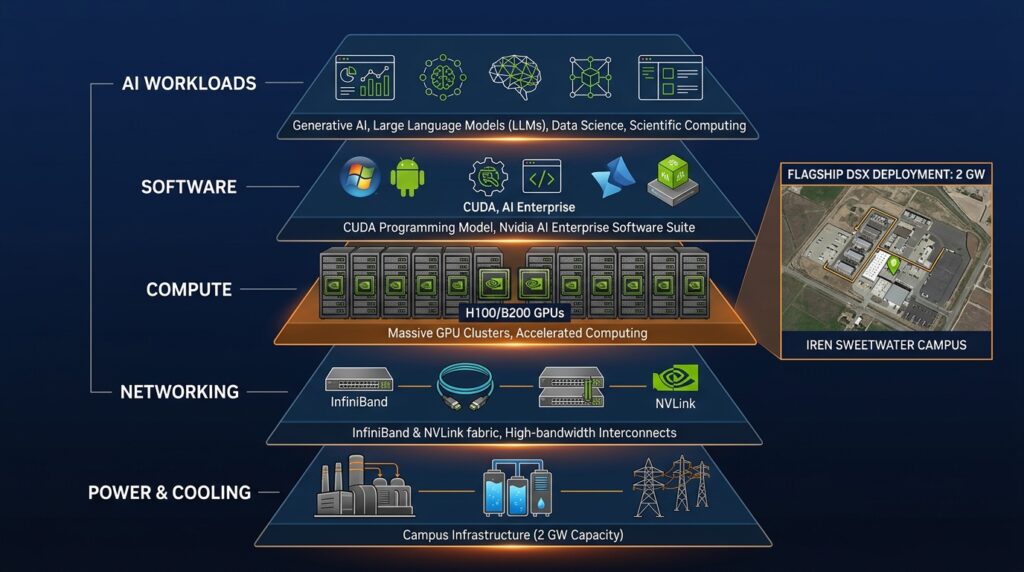

6. The New AI Factory Model – Nvidia’s DSX Architecture and Vertical Integration

The most advanced AI data centers are no longer just server farms. They are integrated “AI factories” —vertically optimized ecosystems combining compute, networking, software, power, and operations.

Nvidia’s DSX (Data Center Scale) reference architecture embodies this new model. The company is not just selling GPUs; it is partnering with operators to deploy complete AI factory environments at utility scale.

The IREN partnership is the most dramatic example. Announced May 7, 2026, the deal positions IREN’s 2 GW Sweetwater campus as a flagship deployment for Nvidia’s DSX architecture. Nvidia secured a five‑year right to purchase up to 30 million shares at 70 per share—a potential 2.1 billion investment—and signed a long‑term cloud services contract for Nvidia’s internal AI workloads.

This vertically integrated approach allows Nvidia to secure dedicated capacity for its own AI training and inference needs, bypassing hyperscalers building their own chips. It is a strategic hedge—and Texas is its anchor.

What This Means for the Future – Challenges and Opportunities

Power Constraints Are Tightening

Texas may have more capacity than Virginia, but it is not infinite. Nearly 40% of planned US data center projects face delays due to power and labor constraints. In May 2026, OpenAI and Oracle shelved a planned 600 MW expansion of the Stargate campus after prolonged financing and operational disagreements, though the existing 1.2 GW facility remains under construction. Curt Holcomb, vice chairman at JLL, noted that most new large loads are now looking at late 2028 and into 2029 for the first increment of new power capacity brought to market by utilities. Developers are increasingly examining behind‑the‑meter generation options.

Water Will Become a Defining Battleground

As the UT Austin report underscores, data center water use could climb to 9% of Texas’ total consumption by 2040. The 2027 Texas legislative session is expected to see fierce debates over water use transparency, alternative sources like reclaimed wastewater, and potential conservation mandates. Developers who lead on water efficiency—like Google with air cooling and Skybox with closed‑loop systems—will have a significant competitive advantage.

Tax Breaks Are Under Review

Data center tax exemptions cost Texas over 1 billion in 2025 and are projected to reach 1 billion in 2025 and are projected to reach 1.8 billion annually by 2030. With the state’s next legislative session convening in January 2027, lawmakers are reconsidering whether this level of incentive spending remains sustainable. Any rollback could slow the pace of new project announcements.

The Global Market Shift

Despite these challenges, the trajectory is clear. Data center vacancy rates held at a record‑low 1% for the second consecutive year in 2026. Nearly two‑thirds of new capacity is being built outside traditional hubs like Northern Virginia and Silicon Valley, and Texas is the biggest beneficiary. The state is on track to overtake Virginia as the world’s largest data center market by 2030—a testament to the power of business‑friendly policies, renewable resources, and sheer available land.

Frequently Asked Questions (FAQ)

Q1: What makes Texas more attractive for AI data centers than Virginia?

A: Power availability. Virginia’s grid is saturated, with interconnection timelines exceeding four years. Texas has abundant renewable and natural gas generation, faster large‑load interconnection processes, and behind‑the‑meter power options. Texas market share surged 142% while Virginia contracted 35%.

Q2: How many data centers does Texas currently have?

A: Texas has approximately 410 existing data center sites (operational and under construction), with 336 planned projects—more than any other state. Over 100 are currently under construction, 142 according to industry data, matching Virginia’s 141.

Q3: How much water do Texas AI data centers consume?

A: Estimates vary. A UT Austin report projects data centers could account for 3–9% of total Texas water use by 2040, up from less than 1% today. However, new closed‑loop cooling systems reduce consumption dramatically. The Stargate campus, despite its massive scale, consumed less than 5% of its water allocation. Google’s upcoming Wilbarger County facility will use no water for cooling at all.

Q4: Is Texas running out of power for all these data centers?

A: Not yet—but constraints are emerging. ERCOT has more capacity than Virginia, but large‑load interconnection timelines are extending. The PUCT’s SB6 rule (March 2026) requires new large‑load customers (75 MW+) to demonstrate readiness and pay upfront fees to prevent speculative projects from clogging the queue. Some developers are building behind‑the‑meter power generation to bypass grid bottlenecks.

Q5: What is the largest AI data center campus in Texas?

A: The Stargate campus in Abilene is designed for up to 1.2 GW and 450,000 Nvidia GB200 Blackwell GPUs, making it one of the world’s largest. Vantage’s Frontier campus (1.4 GW, $25 billion) will be the largest in Vantage’s global portfolio. IREN’s Sweetwater campus is planned for 2 GW with a first phase of 1.4 GW already energized. Microsoft and Crusoe are building an adjacent 900 MW AI factory.

Q6: Will Texas really overtake Virginia as the world’s largest data center market?

A: JLL projects that Texas could overtake Virginia as the largest global data center market by 2030. With 6.5 GW already under construction and the majority of new capacity moving to “frontier markets,” the shift appears structural, not temporary.

Q7: What happens if Texas repeals data center tax breaks?

A: Industry leaders warn that shrinking or ending the tax exemption could “spell an end to Texas’ rising status as the nation’s #1 destination for data centers”. However, the combination of power availability, land, renewable energy, and business climate may still keep Texas competitive even without tax incentives.

Q8: How does the Nvidia‑IREN deal fit into Texas’ AI story?

A: The deal positions IREN’s 2 GW Sweetwater campus as a flagship “AI factory” built to Nvidia’s DSX reference design. Nvidia is expanding beyond chip design into full infrastructure orchestration—and Texas is its anchor market. The 5 GW pipeline across IREN’s global footprint is centered on Sweetwater.

Conclusion – The New Center of AI Gravity

Texas has not become the AI data center capital by accident. It succeeded because it offered what the AI boom demanded most—power, land, speed, and incentives—while established hubs like Virginia ran out of all four.

But the very success that attracted this wave of investment is now straining the state’s resources. ERCOT has new rules for large loads, but grid capacity remains finite. Water has become a political and environmental flashpoint. Tax breaks that once seemed modest now amount to billions of dollars annually, and lawmakers are beginning to ask whether the trade‑off is still worth it.

For now, the momentum is unstoppable. The 6.5 GW under construction today will become 10 GW by decade’s end. The 336 planned projects will reshape rural Texas counties into global hubs of AI compute. And the shift from Virginia to Texas will stand as one of the defining infrastructure trends of the AI era.

The question is not whether Texas will lead. It already does. The question is whether the state can manage the growing pains without breaking the machine that made it the AI capital in the first place.

References & Further Reading

- JLL North America Data Center Report (February 2026)

- UT Austin – Water Requirements for Data Centers in Texas (May 2026)

- Nvidia‑IREN strategic partnership announcement (May 7, 2026)

- Public Utility Commission of Texas – Proposed Rule 16 TAC §25.194 (March 12, 2026)

- Texas State Comptroller – Sales Tax Exemption Report (April 2026)

- Datacenter.fyi / Miner Weekly – Mapping America’s AI Data Center Boom (April 2026)

- Rwazi – US Data Center Market Share Report (April 2026)

- Data Center Knowledge – Vantage Frontier, Microsoft/Crusoe coverage (2025‑2026)

- Bloomberg – OpenAI Stargate expansion pause (May 2026)

- Inside Climate News – Texas data center water use hearing (April 2026)

- Texas Tribune – Data center tax break analysis (April 2026)

If you found this explainer useful, check out our related articles:

👉 Why Nvidia Is Investing Billions to Secure Data Center Capacity (The IREN Deal, Explained)

👉 Why AI & Cloud Infrastructure Demand Is Outpacing Supply (5 Constraints)

👉 Why Google, Microsoft, and Amazon Are Building Their Own AI Chips (6 Reasons)

👉 Why Is Nvidia Still Dominating the AI Chip Market? (7 Moat Factors)

📬 Subscribe to ExplainThisTech for more “why” breakdowns of the technology shaping our world.

Leave a Reply