The End of Cheap AI

Not long ago, many experts confidently predicted that AI compute costs would follow the same curve as every other digital technology: down. Cheaper GPUs, more efficient models, and intense competition would drive prices into the ground.

That prediction has not aged well.

Instead, the opposite is happening. Across the entire AI supply chain – from raw memory chips to cloud GPU rentals – prices are rising, sometimes dramatically. In some cases, they have more than doubled in a single year.

This is not a temporary spike caused by a single event. It is a structural shift driven by demand that far exceeds supply, a physical build‑out that cannot be accelerated, and an economic reality that the AI industry is only now confronting.

This article provides a data‑driven analysis of AI compute costs from 2025 to 2026. You will learn:

- How much GPU rental prices have actually increased (with real numbers)

- Why memory chips (HBM, DDR5) have become the most expensive component in AI infrastructure

- Why prices are not coming down anytime soon – and what that means for your cloud bill

- How to interpret conflicting signals: falling training costs vs. rising inference costs

Let’s start with the most visible part of the AI cost stack: the GPUs themselves.

GPU Rental Prices – H100, H200, and the 38% Spike

The most visible sign of rising AI costs is the price of renting the industry’s most popular workhorse: Nvidia’s H100 GPU.

In 2024, the prevailing wisdom was that GPU prices would fall as supply caught up with demand. That never happened. Instead, as more companies moved from experimentation to production, demand surged, and prices followed.

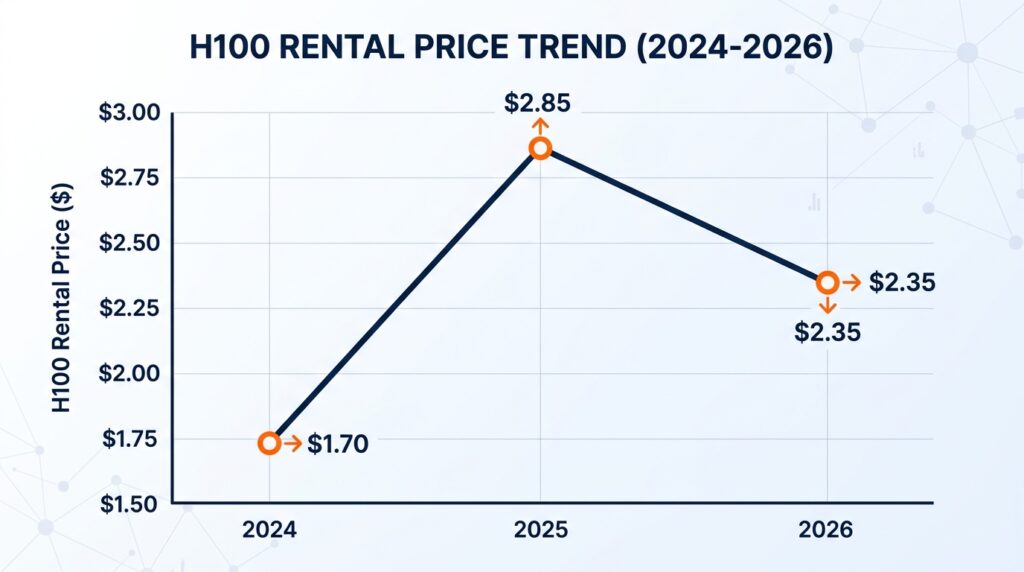

The Numbers

According to industry data from SemiAnalysis and Verified Market Research, the trajectory of H100 rental prices tells a stark story:

| Period | Average Rental Price (per hour) | Change |

|---|---|---|

| 2024 (low) | ~$1.70 | Baseline |

| 2025 (peak) | ~$2.85 | +68% |

| 2026 (current) | ~$2.35 | +38% from 2024 low, but off peak |

While prices have moderated slightly from the 2025 peak, they remain significantly elevated compared to pre‑AI‑boom levels. More importantly, on‑demand capacity is effectively sold out across all GPU types. Even at $2.35 per hour, you cannot simply spin up an H100 instance when you need it—you must commit to long‑term contracts or wait months for capacity.

The situation is even more extreme for newer chips. H200 and B200 instances, where available, command even higher premiums. And Blackwell clusters—Nvidia’s next‑generation platform—have been delayed until at least mid‑2026, further tightening supply.

Why Prices Haven’t Fallen

Three structural factors explain why GPU prices remain stubbornly high:

- Production is sold out. Nvidia’s H100 and B200 production is fully allocated through 2026. There is no spare capacity to bring prices down.

- Demand is price‑inelastic. For hyperscalers and AI labs, the ROI on additional compute is still 5–10x. Even at higher prices, buying more GPUs is a financial winner.

- Inference is exploding. Training gets the headlines, but inference—the ongoing cost of running models—now accounts for roughly two‑thirds of all AI compute. And inference demand grows with every user, every query, every agent.

For enterprises that did not lock in long‑term contracts early, the spot market has become prohibitively expensive. And for startups without deep pockets, the GPU crunch has effectively priced them out of the market entirely.

Memory Prices – The Silent Crisis

While GPU rentals grab headlines, the most dramatic price increases have occurred in a less visible corner of the AI supply chain: memory chips.

For most of 2024 and early 2025, memory prices were stable, even falling. Contract prices for DDR4 and LPDDR5 had dropped for several consecutive quarters. AI demand, the thinking went, was about computation, not storage.

That assumption collapsed in the second half of 2025.

The DRAM Explosion

Starting in late 2025, memory contract prices began an unprecedented climb. By early 2026, the increases had accelerated into what analysts now call a “super‑cycle.”

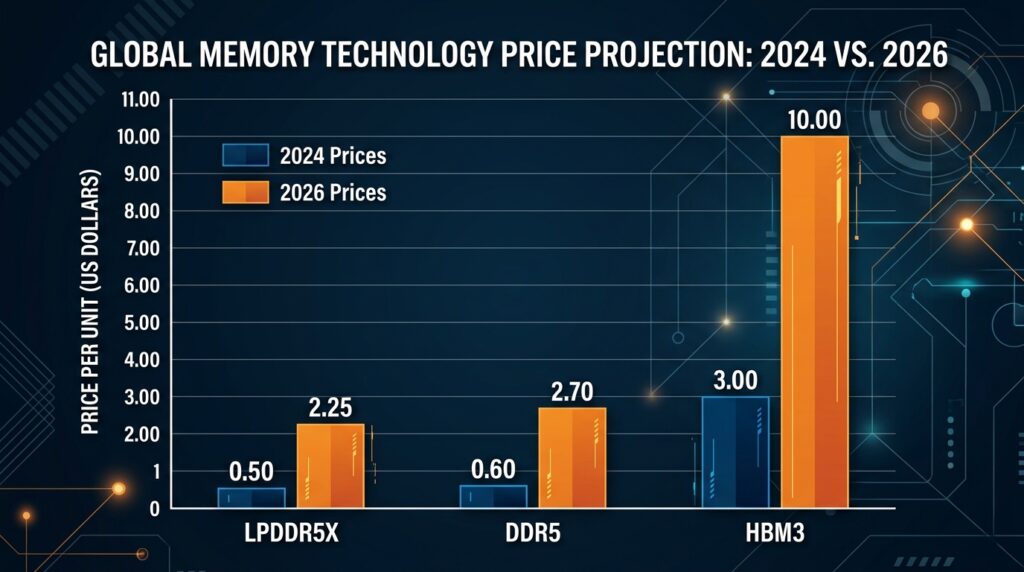

| Memory Type | 2024 Price (per GB) | 2026 Price (per GB) | Increase |

|---|---|---|---|

| LPDDR5X | ~$0.50 | ~$2.00–2.50 | 4–5x |

| DDR5 | ~$0.60 | ~$2.40–3.00 | 4–5x |

| HBM3 | ~$3.00 | ~$10.00 | ~3x |

The numbers are staggering. LPDDR5 and DDR5 contract prices have risen 4 to 5 times year‑over‑year. HBM3 prices have surged 260% , with two‑year cumulative increases exceeding 500%.

Why Memory? The HBM Effect

The driver of this surge is HBM (High‑Bandwidth Memory). Every AI accelerator—Nvidia’s H100, B200, and Rubin; Google’s TPU; AMD’s MI series—requires HBM stacked directly next to the compute die. Without HBM, the fastest GPU is useless.

But HBM production is notoriously inefficient. A single HBM chip consumes 3–4 times the wafer capacity of standard DRAM. As manufacturers shifted capacity to HBM to meet AI demand, they inadvertently starved the market for conventional memory used in PCs, smartphones, and servers.

The result is a simultaneous shortage of both premium HBM and everyday DRAM. Prices for both have skyrocketed in tandem.

HBM4 Negotiations: A Warning for 2027

The situation is about to get worse. Suppliers are already negotiating HBM4 contracts for 2027 delivery, and the early signals are alarming. According to industry sources, memory makers are seeking “severalfold” price increases over already‑elevated HBM3e levels.

If those negotiations succeed, 2027 could see another leg of price increases—just as HBM4 becomes the standard for next‑generation AI accelerators.

The Consumer Impact

The memory shortage is not just an AI problem. PC makers are warning of price hikes for consumer laptops and desktops. Smartphone manufacturers are facing higher component costs. And gamers – already dealing with GPU shortages – now face higher prices for system memory as well.

For enterprises running their own infrastructure, the message is clear: memory is now a line item you cannot ignore. Budgeting for AI compute requires budgeting for memory – and memory prices are no longer stable.

Why Prices Are Staying High – The Structural Analysis

The natural question for anyone watching these numbers is, will prices ever come down? The answer, based on the underlying economics, is not anytime soon.

This is not a temporary supply shock. It is a structural realignment of the AI compute market. Three factors explain why high prices are here to stay.

1. Demand Is Not Price‑Sensitive

In most markets, rising prices reduce demand. Not in AI. For the companies that drive the market—hyperscalers like Amazon, Google, and Microsoft, and AI labs like OpenAI and Anthropic—the return on investment from additional compute remains extraordinary.

Even at current elevated prices, a new GPU cluster can generate 5–10x ROI within months. Until that calculus changes, demand will continue to outstrip supply, regardless of price.

2. Supply Cannot Scale Quickly

Building new semiconductor fabrication capacity takes years. The fabs that will produce HBM4 and next‑generation GPUs are still under construction. They will not deliver meaningful new supply until 2028–2029 at the earliest.

In the meantime, manufacturers face a cruel trade‑off: shifting capacity to HBM (which is needed for AI) means reducing capacity for conventional DRAM (which is needed for everything else). Every new HBM chip comes at the cost of 3–4 standard memory chips.

3. The Inference Explosion Changes the Math

Much of the early discussion about AI costs focused on training—the one‑time expense of building a model. But inference—the ongoing cost of running that model—is rapidly becoming the dominant expense. Gartner projects that inference workloads will account for roughly two‑thirds of all AI compute by 2026.

Unlike training, which is episodic, inference is continuous. Every user query, every agent action, every API call incurs a cost. And as AI agents become more common, the number of inference operations will only grow.

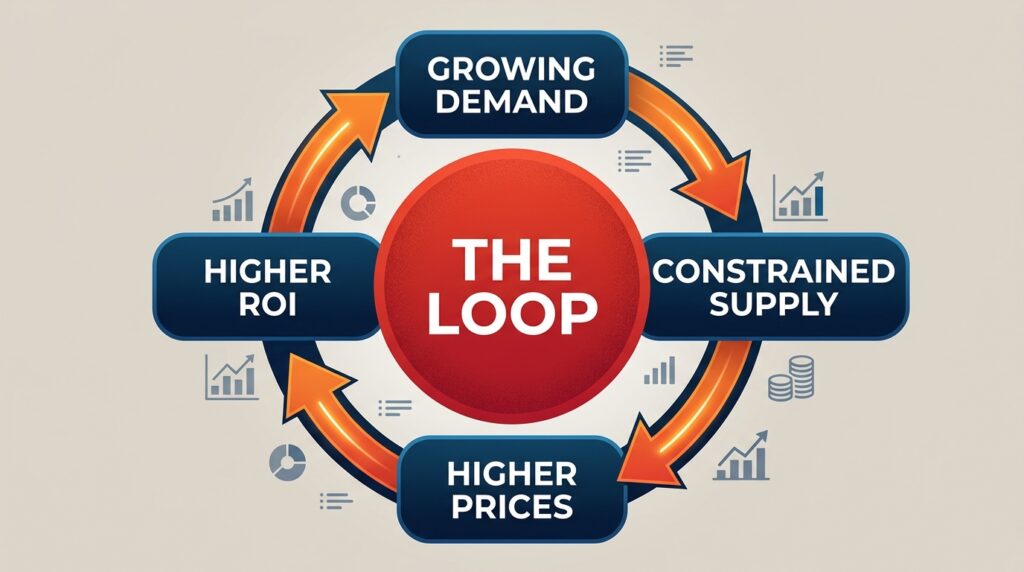

A Self‑Reinforcing Cycle

The combination of these factors creates a self‑reinforcing cycle:

Growing demand → constrained supply → higher prices → higher ROI per chip → even more demand

Breaking this cycle would require either a dramatic slowdown in AI adoption (unlikely) or a technology breakthrough that radically reduces cost per operation (possible, but not imminent).

What This Means for You

For enterprises and developers, the implication is clear: budget for higher costs. The era of cheap, abundant AI compute – if it ever existed – is over. Planning for 2027 and beyond requires assuming that prices will remain elevated and possibly rise further.

For startups, the math is even harder. Without the scale to negotiate long‑term contracts or the capital to pre‑purchase capacity, many are being priced out of the market entirely. The AI industry is consolidating around those with the deepest pockets.

Frequently Asked Questions (FAQ)

Q1: Is now a bad time to buy AI compute?

A: Not necessarily. If you can secure long‑term contracts at current prices, you may be locking in rates that look reasonable in hindsight. But paying spot market prices for on‑demand capacity is increasingly expensive. The best strategy is to commit to capacity well in advance.

Q2: Will HBM4 make prices go down?

A: Unlikely. HBM4 will offer higher performance, but suppliers are already negotiating “several‑fold” price increases over HBM3e. The next generation of memory will be faster—and significantly more expensive.

Q3: Why are memory prices rising faster than GPU prices?

A: Memory production is more constrained. HBM consumes 3–4x the wafer capacity of standard DRAM, and shifting capacity to HBM has created a shortage of conventional memory. GPU production, while also constrained, has received more investment and attention.

Q4: Should I switch to smaller, more efficient models?

A: Yes. Many organizations are finding that smaller models (e.g., Llama 3 8B, Mistral 7B) can handle the majority of their inference tasks at a fraction of the cost. Saving the largest models for only the most complex queries is a sound cost‑control strategy.

Q5: How does inference cost compare to training cost?

A: For most organizations, inference is now the larger expense. Training is a large one‑time cost; inference is a continuous expense that scales with usage. For popular models serving millions of users, monthly inference costs can exceed the original training cost within weeks.

Q6: Will prices ever come back down?

A: Eventually, yes – but not soon. New fabrication capacity will come online in 2028–2029, and competition from custom chips (Google’s TPU and Amazon’s Trainium) may put downward pressure on Nvidia’s pricing. But for the next 2–3 years, high prices are the new normal.

Q7: How does this connect to your earlier article on the Microsoft/Uber cost crisis?

A: Directly. The Microsoft and Uber stories were early warning signs of the broader trend. Microsoft canceled Claude Code licenses because token costs were spiraling. Uber burned through its AI budget in four months. This article provides the underlying data that explains why those cost overruns happened—and why they will continue.

Q8: What should a startup do to manage AI costs?

A: Optimize relentlessly. Use smaller models where possible. Cache inference results. Negotiate long‑term capacity commitments. And consider alternative providers—not just the big three cloud vendors, but specialized “neoclouds” that may offer better pricing for specific workloads.

Conclusion – The Age of Cheap AI Is Over

The data is unambiguous. Across the entire AI supply chain – from memory chips to GPU rentals – prices are rising, not falling. H100 rental rates are up 38% from their 2024 lows. HBM prices have surged 260%. LPDDR5 and DDR5 contract prices have increased 4 to 5 times year‑over‑year.

This is not a temporary spike. It is a structural shift driven by demand that far exceeds supply, a physical build‑out that cannot be accelerated, and an economic reality that the AI industry is only now confronting.

For the past two years, many in tech operated under an implicit assumption: compute would get cheaper over time, just as storage and bandwidth had before it. That assumption is now broken.

The implications are profound. For hyperscalers, the challenge is managing costs without slowing innovation. For enterprises, the challenge is budgeting for a line item that is no longer predictable. For startups, the challenge is survival—finding a path to profitability in an environment where every query, every agent, and every inference has a real and rising cost.

The age of cheap AI is over. Welcome to the age of expensive intelligence.

Sources & Further Reading

1. GPU Rental Prices (Section 2)

- SemiAnalysis – GPU market pricing analysis, 2025‑2026

- Verified Market Research – H100 rental rate trends

- Industry reporting on Blackwell cluster delays (mid‑2026)

2. Memory Prices (Section 3)

- TrendForce – DRAM and NAND contract price reports, Q1‑Q2 2026

- Counterpoint Research – HBM market analysis, 2025‑2026

- Industry reporting on HBM3 pricing surges (260%+, 500% cumulative)

- Analyst reports on LPDDR5X and DDR5 contract price increases (4‑5x YoY)

3. Structural Analysis (Section 4)

- Gartner – Inference vs. training workload projections (2025‑2026)

- J.P. Morgan – AI supply‑demand outlook (April 2026)

- SK Hynix / Samsung / Micron – Public commentary on capacity constraints

- Industry reporting on HBM4 price negotiations (“several‑fold” increases)

4. Supporting Context

- Microsoft / Uber AI cost crisis reporting (May 2026)

- Nvidia Q1 FY2026 earnings report and commentary

- TSMC – Capacity expansion timelines (2026‑2029)

Leave a Reply