The Trillion-Dollar Inflection Point

Ask any CTO two years ago what kept them up at night, and the answer was the same: where to hire enough data scientists to build their own foundation model. That conversation feels almost quaint now. Today, the anxiety is over integration, ROI, and above all, scale.

Quick Takeaways

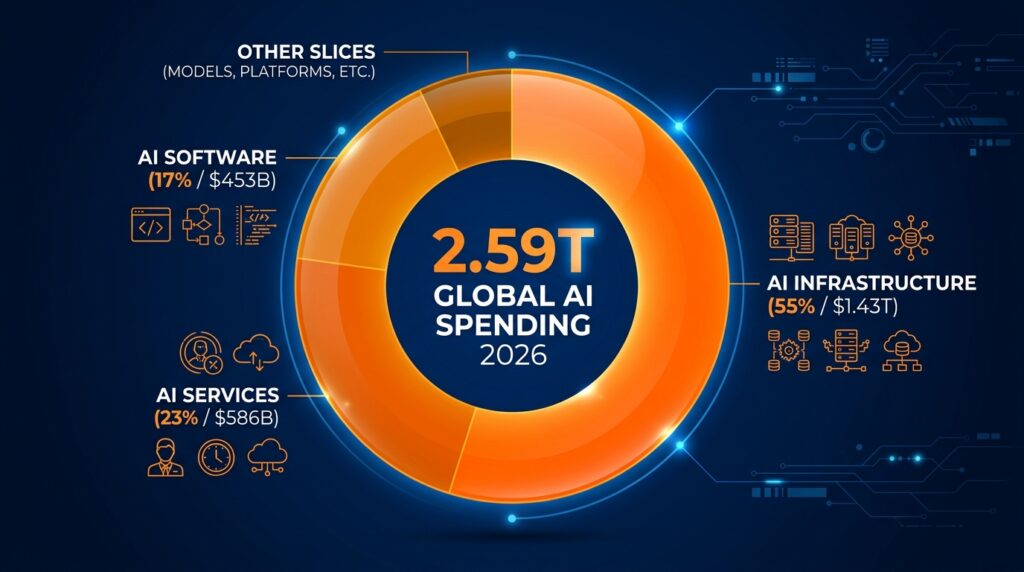

- AI spending will hit 2.59 trillion in 2026—up 471.43% (55% of total).

- Enterprises are finally moving from pilots to production – after years of experimentation, 2026 is the inflection year where AI is embedded into core business workflows.

- Software is the fastest‑growing segment – up 60% year‑over‑year, as companies buy, fine‑tune, and deploy AI capabilities rather than building from scratch.

- Inference has overtaken training – inference workloads now account for two‑thirds of AI compute, driven by always‑on agents and real‑time applications.

- Agentic AI is multiplying costs – recursive agent loops can generate thousands in unplanned compute per incident, with an estimated $400 million annual burn from such failures.

- Infrastructure remains the bottleneck – power, chip supply, transformer shortages, and construction delays continue to throttle new capacity, even as budgets soar.

- Only 12% of CEOs report both revenue growth and cost savings from AI – the ROI picture is still uneven, and governance – not technology – separates winners from laggards.

- 40% of enterprise apps will embed task‑specific AI agents by end of 2026 – up from less than 5% in 2025, marking an eight‑fold increase.

- The talent wall is real – the shortage of data engineers, MLOps specialists, and change‑management leaders is the single biggest risk to sustained growth.

- The production era has begun – the shift from “chat” to “act” is no longer a prediction; it is a line item on enterprise budgets.

For all the hype, the AI era has largely been a story of vendors and hyperscalers. They spent the money, they built the data centers, they trained the models. Enterprises, by and large, watched from the sidelines. That changes now.

Gartner’s latest forecast projects global AI spending to reach 2.59 trillion in 2026, a 473.49% increase.

But the more significant headline is the shift in who is spending. Through 2025, AI investment was almost entirely infrastructure‑driven—vendors like Nvidia, cloud providers like AWS, and the companies that supply them. That era is ending. 2026 is the year enterprises finally flex their spending potential, moving AI from labs and pilots into production workflows, customer‑facing applications, and the core of business operations.

That shift—from “experiment” to “engine”—is what this article unpacks. We’ll examine where the $2.6 trillion is going (and how it is now being spent), explore why enterprises are finally ready to deploy at scale, trace the tectonic pivot from training to inference, and highlight the cracks in the foundation that could slow the rollout.

The Numbers – A $2.6 Trillion Market Takes Shape

1.1 The Top‑Line Forecast

Global AI spending is projected to hit 2.59 trillion in 2026, up 471.76 trillion in 2025. By 2027, Gartner expects the market to reach $3.49 trillion. To put that in perspective: AI spending alone will soon exceed the entire IT budgets of most nations.

1.2 Where the Money Is Going – The Infrastructure‑First Reality

For all the talk of software and agents, the largest single category remains AI infrastructure —including optimized servers, networking fabric, processing semiconductors, and IaaS. This segment alone is forecast to hit $1.43 trillion in 2026, accounting for over 55% of all AI spending and growing at a compound annual rate that far outstrips the rest of the market.

The driver is simple: model creators and cloud providers are making a massive upfront bet that the workloads are coming. Gartner’s John‑David Lovelock noted that “through the next several years, the need for capacity will make AI infrastructure the largest segment of the market, driven by vendors”. Within that, AI‑optimized servers will triple over the next five years as hyperscalers scramble to build out capacity for the coming wave of agentic workflows.

1.3 Where the Money Is Starting to Go – The Enterprise Pivot

The most telling number is not the infrastructure total but the change in growth rates:

| Category | 2026 Spending | Growth vs. 2025 |

|---|---|---|

| AI Software | $453B | +60% |

| AI Services | $586B | +34% |

| AI Infrastructure | $1.43T | +47% |

Software is the fastest‑growing segment, up 60% from the prior year, as enterprises start embedding AI capabilities into existing workflows rather than building them from scratch. For CIOs, the dam has broken. After two years of cautious pilots, the question is no longer “should we?” but “how fast can we?”

As Gartner’s Lovelock put it: “Up to this point, AI spending has primarily been driven by technology companies and hyperscalers. Enterprises have yet to really flex their spending potential. That is coming and 2026 will be the inflection year”.

From Pilot to Production – Why Enterprises Are Finally Ready

If 2025 was the year of the pilot, 2026 is the year of production. Several factors have converged to push AI from the lab to the core of business operations.

2.1 The Agentic Tipping Point

For two years, “AI agent” was a buzzword in search of a product. No longer. Gartner predicts that by the end of 2026, 40% of enterprise applications will be integrated with task‑specific AI agents, up from less than 5% in 2025. That is an eight‑fold increase in a single year.

These are not chatbots answering customer questions. They are agents embedded in finance, HR, supply chain, and sales workflows, handling specific tasks with defined boundaries and measurable outcomes.

IDC forecasts that by 2027, nearly half of enterprises will rely on AI agents to redefine human‑machine collaboration, with large‑scale enterprise adoption accelerating significantly through 2026.

2.2 The Democratization of AI Tools

One reason for the slow start was complexity. Building a custom model required PhDs and millions in compute. Deploying one required armies of engineers. That barrier has collapsed.

Model costs have dropped precipitously (public cloud API prices fell nearly 80% year‑over‑year), and turnkey tools have proliferated. Enterprises no longer need to build their own foundation models. They can buy, fine‑tune, and embed capabilities that were science projects 18 months ago.

2.3 The ROI Imperative

The existential driver, however, is pressure. The 2026 macroeconomic environment leaves no room for vanity projects. Lovelock noted that “currently, organizations show limited appetite for using AI to drive disruptive enterprise change. Instead, they favor tactical AI initiatives with incremental improvements in efficiency and productivity”.

That incrementalism is not a bug; it is the path to scale. Small wins—20% faster claims processing, 30% reduction in manual data entry—build the case for larger deployments.

Yet the pressure to deliver value is not being met uniformly. PwC’s 29th Global CEO Survey of 4,454 chief executives found that 56% report AI has produced neither increased revenue nor decreased costs; only 12% have achieved both. The differentiator, PwC found, was governance architecture—not which model they chose, but how they embedded it.

2.4 The Infrastructure Gap

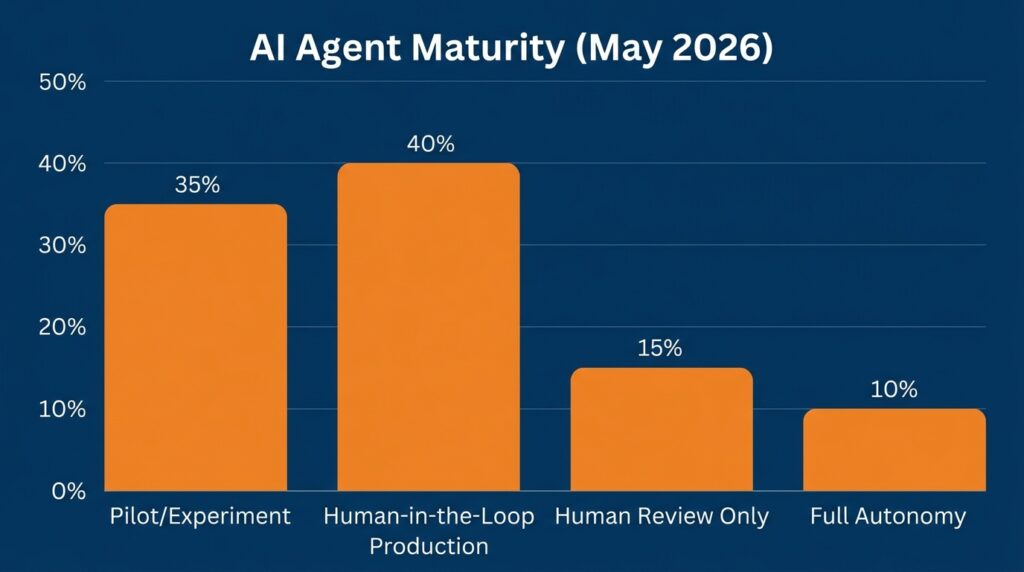

For all the enthusiasm, the physical reality remains daunting. The number of enterprises with AI agents in fully autonomous production is still only 10%, with 40% still using human review of agent outputs. The gap between “capable” and “trustworthy” remains wide.

CIOs also face challenges proving the value of AI investments and demonstrating tangible business outcomes. Lovelock warned that “aligning AI initiatives with strategic business objectives is the essential step for success”. The technology is ready; the organizational muscle is still developing.

The Economics Are Flipping – Inference Overwhelms Training

The shift from experimentation to production has a subtle but profound implication for where AI dollars actually land.

3.1 The End of the “One‑Time Cost” Myth

For years, the headline number was training cost: 100 million for GPT‑4,500 million for whatever comes next. Training is episodic. It happens a few times a year, and when it is done, the spend stops.

Inference is different. Inference runs every time a user asks a question, an agent executes a task, or a workflow processes a document. It is a utility, not a project—continuous, scaling with usage, and often invisible until the bill arrives.

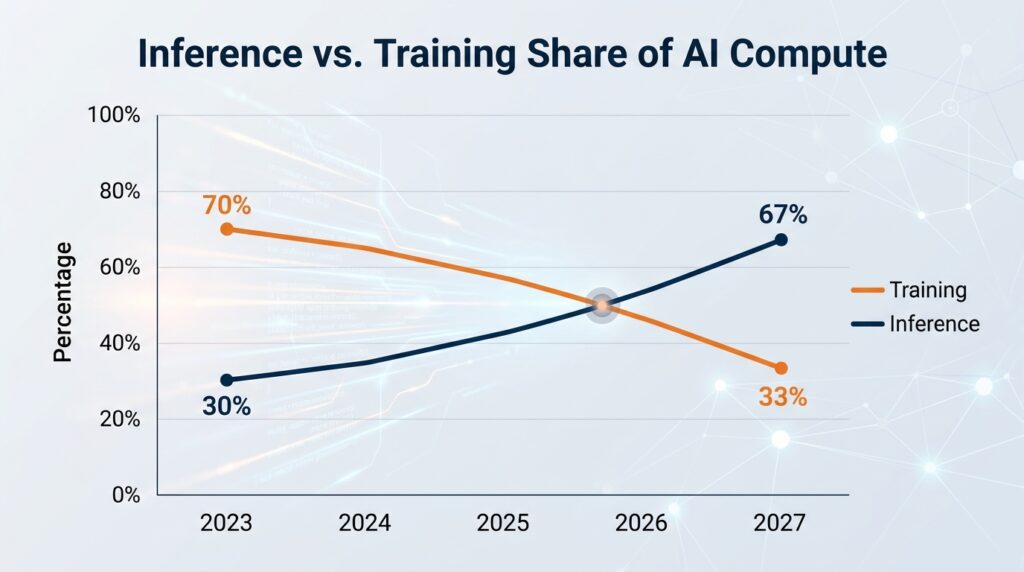

Inference workloads are now set to overtake training as the dominant AI compute category. Deloitte Tech Trends 2026 estimates that inference will account for two‑thirds of all AI compute this year.

3.2 The Numbers Behind the Flip

The data is consistent across surveys. DigitalOcean’s Currents report, drawn from over 1,100 responses from developers, CTOs, and founders, found that nearly half (44%) of organizations now allocate the majority (76‑100%) of their AI budget to inferencing, rather than training.

A separate industry analysis found that inference at scale represents 34.6% of enterprise AI compute consumption, while training large foundation models accounts for 24.9%, training domain‑specific models consumes 23.3%, and fine‑tuning existing models utilizes 17.2%. The shift away from pure “train from scratch” and toward “train once, infer endlessly” is already well underway.

| Workload Type | Share of Enterprise AI Compute |

|---|---|

| Inference at scale | 34.6% |

| Training large foundation models | 24.9% |

| Training domain‑specific models | 23.3% |

| Fine‑tuning existing models | 17.2% |

The infrastructure consequences are massive. Inference‑optimized hardware, edge deployment, and cost management tools are becoming urgent priorities. Training was about raw speed; inference is about efficiency, latency, and unit economics.

3.3 The Agentic Cost Amplifier

The shift to inference is not the only cost pressure. The rise of agentic AI—autonomous agents that run in recursive loops—multiplies inference consumption in ways that neither budgets nor guardrails have fully absorbed.

A single three‑hour recursive loop can generate approximately $3,700 in unplanned compute costs before any guardrail activates. If attendant agents run simultaneously, that figure skyrockets to $37,000 per incident. In fact, Analytics Week estimates that recursive loop failures alone absorb roughly $400 million annually across the industry.

These are not theoretical problems. They are line items on cloud bills today—and they are growing faster than any CFO’s forecasting model.

The Winners and Losers – A New Competitive Map Emerges

As spending patterns shift, so does the balance of power.

4.1 Infrastructure Vendors Continue to Dominate (For Now)

Nvidia remains the most obvious beneficiary. The company’s latest quarterly revenue of $81.6 billion far exceeded expectations, driven entirely by data center demand that shows no signs of slowing.

But the infrastructure landscape is not static. The segment that grew fastest in Gartner’s forecast was not chips but AI‑optimized servers, a space where Dell, HPE, Supermicro, and a host of other vendors are racing to build offerings tailored to inference workloads—often using Nvidia’s chips but capturing more of the value stack.

4.2 The “Neoclouds” Rise

The most interesting development is the emergence of specialized AI infrastructure providers—CoreWeave, Crusoe, Nebius, and others—that have built their entire business models around serving inference‑heavy, production‑scale workloads. Unlike AWS or Azure, which must serve general‑purpose cloud customers, these neoclouds can optimize every layer for AI.

Goldman Sachs estimates that the AI infrastructure market has already begun to bifurcate, with enterprises choosing between hyperscalers for breadth and neoclouds for specialized price‑performance. The winners will be those that can deliver both.

4.3 The First Mover Advantage in Agents

On the software side, the 40% adoption forecast is not evenly distributed. Enterprises that began deploying agents early—Microsoft with Copilot, Salesforce with Einstein, ServiceNow with Now AI—have built substantial leads in both technical integration and user training.

Later entrants face steeper adoption curves, not because the technology is worse, but because organizational change takes time. The agent vendors that embedded themselves in core workflows in 2024 and 2025 will be difficult to displace.

The Roadblocks – Why the Inflection Point Is Not a Straight Line

For all the growth, significant obstacles remain.

5.1 The Talent Wall Remains

AI spending forecasts assume that enterprises can hire the people to build and run these systems. The data suggests otherwise. While foundational model training has become centralized in a handful of labs, the demand for data engineers, ML ops specialists, and infrastructure architects is exploding.

The talent gap is not just about technical skills. The organizations that succeed in 2026 are not those with the most powerful models; they are those with the most effective governance, FinOps, and change management structures. The technology is ready. The organizations are not.

5.2 The Infrastructure Crunch

Gartner’s $1.43 trillion infrastructure forecast assumes that chips, servers, and data centers can be built fast enough. The physical realities suggest otherwise. Power constraints, transformer shortages, water consumption, and construction timelines continue to delay new capacity. Nvidia’s GPUs are sold out through 2027, and new fabs take years to bring online.

The gap between announced spending and deliverable capacity is widening, and 2026 will be the year that gap becomes impossible to ignore.

5.3 The ROI Conundrum

PwC’s finding that only 12% of CEOs report both revenue growth and cost savings from AI is a flashing yellow light. Enterprises are deploying, but they are not yet seeing the bottom‑line impact that would justify the next wave of investment.

The risk is that disappointed CFOs pull back, slowing the shift from pilot to production before it fully takes hold. Lovelock cautioned that “CIOs face challenges in proving the value from AI investments” and that “this incremental approach persists despite AI hype”.

The 2026 inflection point is real, but it is not guaranteed to sustain.

Frequently Asked Questions (FAQ)

Q1: Is the $2.59 trillion number for 2026 real spending or just hype?

A: It is a forecast based on actual procurement and contract data from Gartner. Whether those dollars translate into economic value is a separate question. The spending is happening. The returns are still uncertain.

Q2: Why is infrastructure still the largest category if enterprises are deploying software?

A: Because the software runs on hardware. Every new AI application, every deployed agent, every inference query consumes compute. The infrastructure spend is a leading indicator of the deployment wave to come.

Q3: How does this connect to your earlier article on Nvidia’s $81.6 billion quarter?

A: Directly. Nvidia is the largest single infrastructure vendor. Its record results are the clearest signal that the 2026 inflection point is already underway. But as this article shows, the enterprise spending wave is just beginning.

Q4: What is “agentic AI” and why does it matter for spending?

A: Agentic AI refers to autonomous agents that can plan, act, and adapt across multiple steps and tools without constant human supervision. It matters because agents consume inference continuously, not episodically, shifting the cost profile from projects to utilities.

Q5: Which industries are spending the most on AI?

A: Gartner’s forecast does not break out verticals, but the fastest growth is in industries where document processing, customer interaction, and compliance review are core functions: financial services, insurance, healthcare, and professional services.

Q6: Is the inference shift good or bad for cloud providers?

A: Both. Inference workloads are more stable and predictable than training, which is good for capacity planning. But they are also more price‑sensitive, putting pressure on margins.

Q7: What happens if the infrastructure crunch worsens?

A: If new capacity cannot be built fast enough to meet inference demand, prices will rise, deployment timelines will lengthen, and some enterprises may delay production rollouts. The 47% spending growth forecast assumes that supply can keep pace.

Q8: When will enterprise AI spending surpass infrastructure spending?

A: Not in the next several years. Gartner projects infrastructure to remain the largest category through at least 2027. But the fastest growing segment is software (60% YoY), and if that pace continues, the crossover could occur in the early 2030s.

Conclusion – The Inflection Year

2026 is not the year AI becomes a mature market. It is the year the market transitions. Billions will be spent on infrastructure that will not be fully utilized until 2027 or later. Hundreds of thousands of enterprise applications will embed AI agents that are still learning to be reliable. Inference costs will surprise CFOs, and talent gaps will slow deployments.

Yet the direction is unmistakable. After years of hype and pilot projects, AI is finally moving into the core of business operations. The $2.59 trillion forecast is not a prediction of smooth sailing. It is a forecast of enormous investment, messy deployment, and uneven returns.

The technology is ready. The economics are shifting. The organizations that master governance, cost management, and organizational change will reap the rewards. Those that treat this as a technology project rather than a business transformation will watch from the sidelines—again.

The pilot era is over. The production era has begun.

References & Further Reading

- Gartner – “Forecast: AI Spending, Worldwide, 2025‑2030” (May 19, 2026)

- DigitalOcean – “Currents Report: February 2026” (survey of 1,100+ developers, CTOs, founders)

- Deloitte – “Tech Trends 2026”

- PwC – “29th Global CEO Survey” (N=4,454)

- CIO.com – “The inference bill nobody budgeted for” (April 2026)

- Gartner – “Predicts 40% of Enterprise Apps Will Feature Task‑Specific AI Agents by 2026” (August 2025)

- Financial Times – “Enterprise AI spending finally set to surpass infrastructure” (May 2026)

Leave a Reply