The AI Engine That Never Stops

Every quarter, Wall Street waits for Nvidia to stumble. Every quarter, Nvidia proves them wrong.

On Wednesday, the chip giant reported its fiscal first‑quarter 2026 results, and the numbers were staggering: 81.6 billion in revenue, an 8579.2 billion. Net income more than tripled to $58.3 billion.

Yet, in the hours after the announcement, Nvidia’s stock slipped nearly 1%. The reaction was not a sign of failure — it was a symptom of a company that has become a victim of its own success. When investors expect perfection, merely being excellent is no longer enough.

Quick Takeaways

- NVIDIA reported a record $81.6 billion in quarterly revenue, up 85% year-over-year.

- Data center revenue surged to $75.2 billion, showing how AI infrastructure now dominates Nvidia’s business.

- Nvidia announced an enormous $80 billion stock buyback alongside a 25x dividend increase.

- Despite record earnings, Nvidia’s stock barely moved because investors already expected near-perfect results.

- High-Bandwidth Memory (HBM) shortages remain the biggest bottleneck limiting AI hardware growth.

- Nvidia’s upcoming “Vera Rubin” AI platform faces some delays and lower-than-expected HBM4 speeds.

- Demand for AI chips remains so strong that Nvidia still projected $91 billion in Q2 revenue.

- Hyperscalers like Google, Amazon, and Microsoft are developing custom AI chips to reduce dependence on Nvidia.

- Nvidia’s biggest long-term advantage remains its CUDA software ecosystem and full-stack AI infrastructure dominance.

- The earnings report confirms that the global AI boom is still accelerating — and Nvidia remains at the center of it.

This article breaks down Nvidia’s record‑breaking quarter, why the market yawned, how the company is navigating supply chain chaos and geopolitical headwinds, and what the $80 billion buyback and 25x dividend increase mean for shareholders.

The Numbers – A Quarter for the History Books

Revenue and Profit

| Metric | Q1 2026 | YoY Change |

|---|---|---|

| Total Revenue | $81.6 billion | +85% |

| Net Income | $58.3 billion | +210% |

| Data Center Revenue | $75.2 billion | +92% |

| Gaming Revenue | $4.1 billion | +12% |

| Professional Visualization | $1.2 billion | +18% |

| Automotive | $1.1 billion | +15% |

Data center revenue now accounts for over 92% of Nvidia’s total revenue, underscoring the company’s complete transformation from a gaming GPU maker to an AI infrastructure powerhouse.

Cash and Capital Return

- 80 billion new share repurchase authorization–on top of 38.5 billion remaining from prior programs.

- Quarterly dividend raised from 0.01 to 0.01 to 0.25 per share – a 25‑fold increase.

- Approximately $20 billion returned to shareholders in Q1 alone.

Why the Stock Barely Moved – The Paradox of Perfection

Nvidia delivered an extraordinary quarter. So why did the stock trade flat?

The Bear Case: Priced for Perfection

- Sky‑high expectations – Beating estimates is now the baseline. A mere beat no longer triggers a rally.

- Supply constraint concerns – News that the upcoming “Vera Rubin” platform will use slower HBM4 memory than originally planned (20 TB/s vs. 22 TB/s target) spooked some investors.

- Rubin delays – The highest‑end Rubin chips will ship later than expected, raising questions about the pace of Nvidia’s next‑generation ramp.

The Bull Case: A Cash Machine Beyond Compare

- 400 billion annual run rate—Analysts estimate Nvidia’s full‑year 2026 revenue could approach 400 billion, up from just ~$27 billion in 2022.

- Unmatched capital return – The $80 billion buyback and 25x dividend increase signal immense confidence in future cash flows.

- Q2 guidance – Nvidia projected $91 billion in revenue for Q2 2026, well above analyst estimates, demonstrating sustained demand for Blackwell GPUs.

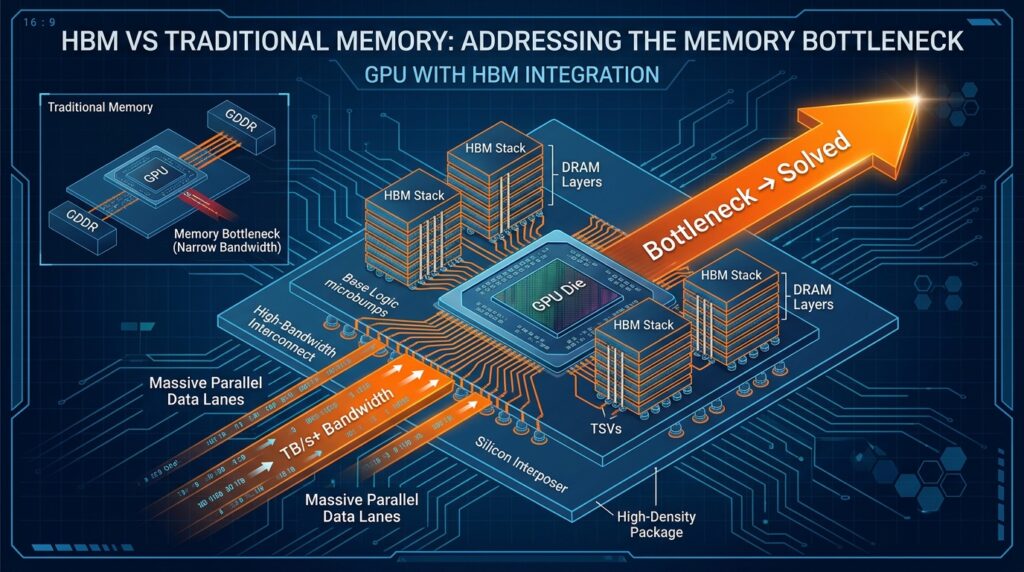

The Supply Chain Brilliance – HBM, Samsung, and Rubin

Nvidia’s growth is gated by one thing: High‑Bandwidth Memory (HBM). How the company manages this bottleneck reveals its strategic genius.

The HBM Squeeze

HBM is the ultra‑fast memory stacked next to Nvidia’s GPUs. It is the single scarcest component in AI hardware. All major HBM suppliers — SK Hynix, Samsung, Micron — are sold out through 2026.

Forcing Samsung’s Hand

According to industry sources, Nvidia pressured Samsung to repurpose a major DRAM production line from conventional memory to the more advanced, higher‑margin HBM category. This is a strategic masterstroke: Nvidia is effectively dictating its suppliers’ capacity allocation.

The Rubin Reality Check

Nvidia’s next‑generation “Vera Rubin” platform will use HBM4 memory running at 20 TB/s — still blistering, but below the originally targeted 22 TB/s. High‑end Rubin adoption has also been pushed back several months. Yet Nvidia raised its revenue forecast anyway, demonstrating that demand far outstrips any temporary supply hiccups.

Geopolitics and Strategy – China, ARM, and SoftBank

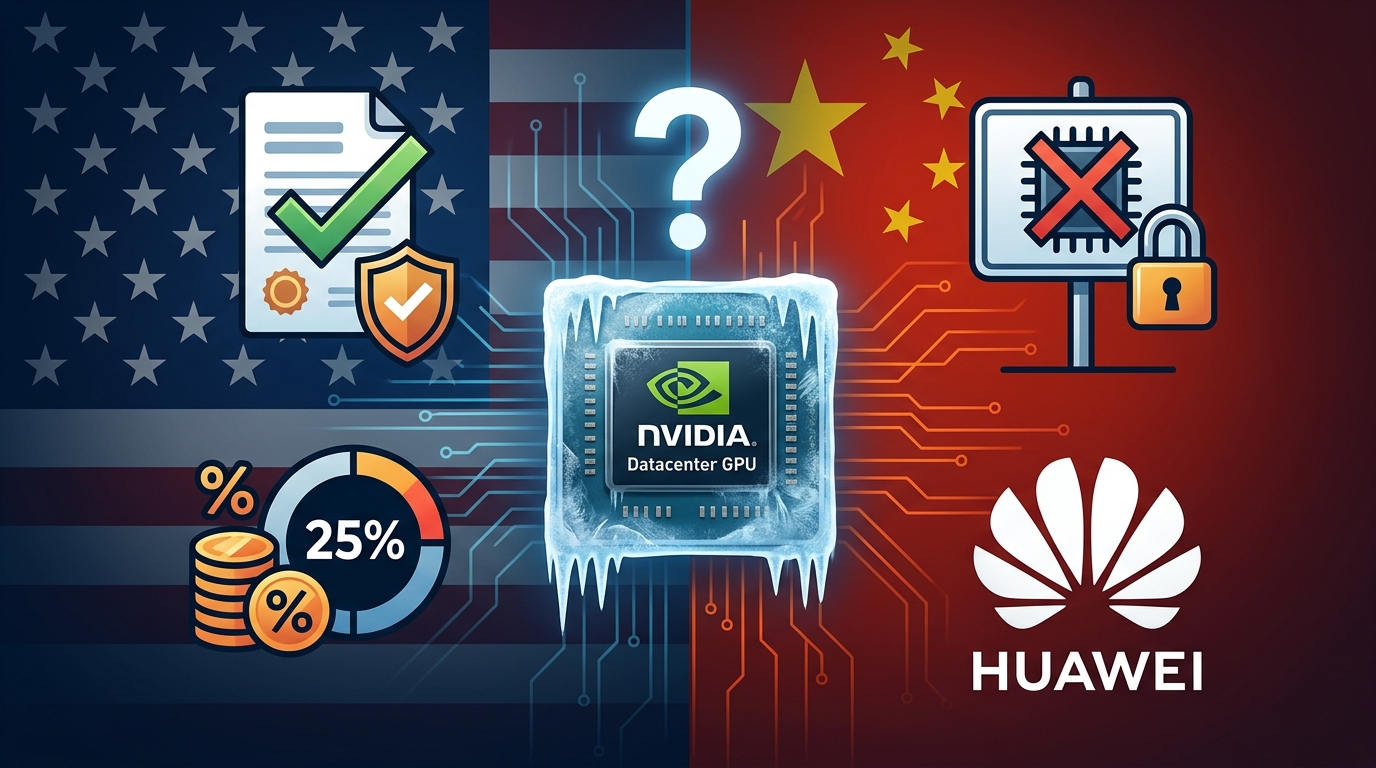

The China Conundrum

US export controls have cratered Nvidia’s sales to China. The company cannot ship its most advanced chips to Chinese customers. But the data center revenue numbers tell the story: demand from the rest of the world has more than compensated. Nvidia has proven it can thrive without the China market — though the lost opportunity remains massive.

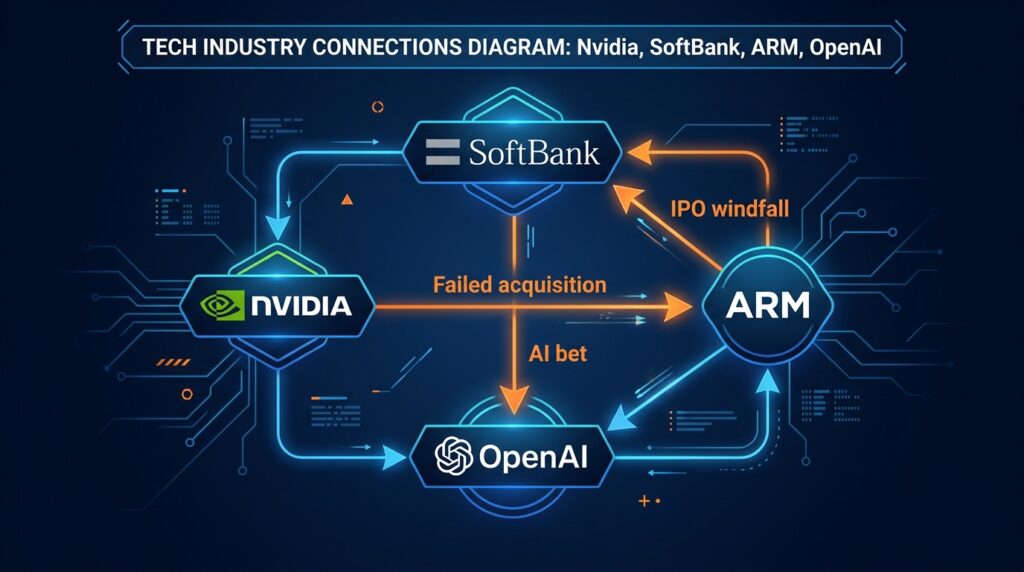

Exiting ARM: A Strategic Victory Disguised as Defeat

Nvidia formally closed the door on its failed $40 billion acquisition of ARM by selling its entire stake. The deal was blocked by regulators in 2022. But ARM’s subsequent IPO has been a massive success, and SoftBank — ARM’s majority owner — has reaped the rewards.

SoftBank’s 20% Surge – The Unseen Winner

SoftBank’s stock jumped 20% on Nvidia’s earnings. Why? Because the Japanese investment giant is tied to Nvidia in three ways:

- The ARM IPO payoff – Nvidia’s failed acquisition forced SoftBank to take ARM public, raising billions while retaining control of a now‑much‑more‑valuable asset.

- The Stargate bet – SoftBank has committed tens of billions to the “Stargate” AI infrastructure project alongside OpenAI and Oracle.

- OpenAI stake pursuit – SoftBank is reportedly looking to acquire up to 1% of OpenAI, betting on the AI boom from every angle.

The Competitive Landscape – Hyperscalers and Neoclouds

Nvidia’s dominance is not unchallenged.

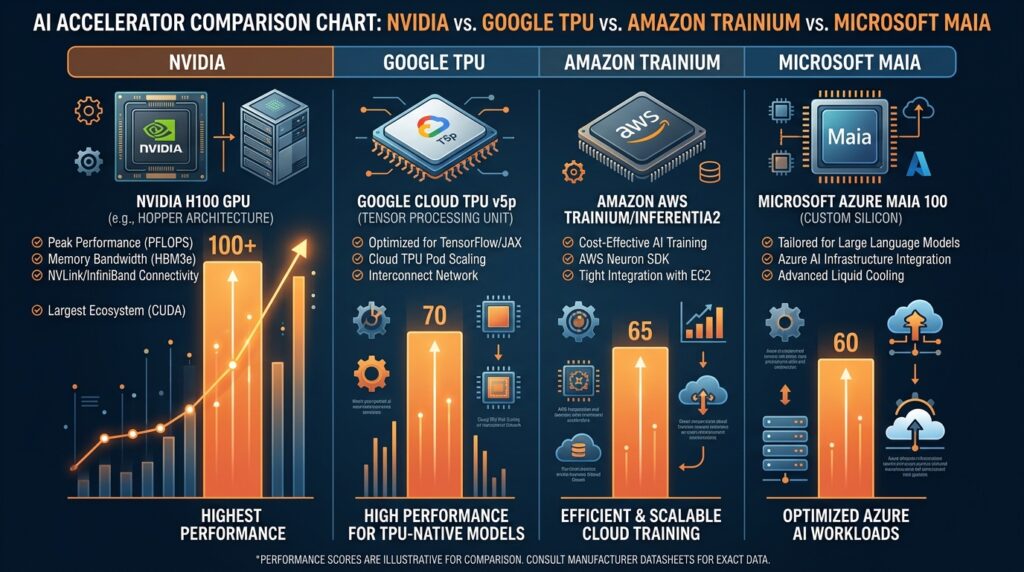

Hyperscaler Custom Chips

Google (TPU), Amazon (Trainium/Inferentia), and Microsoft (Maia) are all building their own AI chips. In the short term, none can match Nvidia’s performance or software ecosystem (CUDA). But over the next 3–5 years, these in‑house alternatives could erode Nvidia’s market share.

The Rise of Neoclouds

Specialized AI cloud providers — CoreWeave, Nebius, Akamai — are winning business by offering better price/performance and faster access to Nvidia’s latest chips. Nvidia has even invested in some of them (CoreWeave, Nebius, IREN), effectively hedging its bets.

Nvidia’s Moat Remains Formidable

- CUDA software ecosystem – Still the industry standard, with no near‑term challenger.

- Full‑stack integration – Chip → server → networking → software. No competitor offers a complete package.

- Supply chain control – Nvidia dictates terms to memory suppliers and has preferential access to TSMC’s advanced packaging.

What the $80 Billion Buyback Means for Investors

Nvidia’s capital return program is unprecedented for a company still growing at 85% annually.

Why Buy Back Stock Instead of Investing More?

- Limited supply – Nvidia cannot spend its way out of HBM or packaging bottlenecks. Cash cannot accelerate TSMC’s fab construction.

- Shareholder reward – Returning cash to investors signals confidence that the stock is undervalued.

- Offsetting dilution – Employee stock compensation dilutes shares. Buybacks neutralize that effect.

The Dividend Message

Raising the quarterly dividend from 0.01 to 0.25 — a 25‑fold increase — sends a clear signal: Nvidia is not a growth‑at‑all‑costs startup anymore. It is a mature, cash‑generating behemoth that intends to reward long‑term holders.

Could Nvidia Eventually Hit an AI Wall?

For now, NVIDIA remains the undisputed king of the AI hardware market. But even the world’s most valuable AI company faces limits — and some analysts believe Nvidia could eventually run into an “AI wall.”

Power Grid Limits

The AI boom is consuming electricity at an astonishing pace. Modern AI data centers require enormous amounts of power to run tens of thousands of GPUs continuously. In some regions, utilities are already struggling to provide enough electricity for new AI facilities.

Major technology companies are now racing to secure:

- dedicated power agreements,

- nuclear energy partnerships,

- and long-term grid capacity.

If electricity infrastructure cannot scale fast enough, AI growth itself could slow down — regardless of how many chips Nvidia produces.

Hyperscalers Want Independence

Today, companies like Microsoft, Google, and Amazon still rely heavily on Nvidia GPUs. But they are also investing billions into their own custom AI chips.

Examples include:

- Google TPU

- Amazon Trainium and Inferentia

- Microsoft Maia

These hyperscalers want greater control over:

- AI costs,

- supply chains,

- and infrastructure optimization.

Over time, vertical integration could reduce Nvidia’s dominance, especially if custom chips become “good enough” for many workloads.

CUDA Alternatives Are Slowly Emerging

One of Nvidia’s greatest strengths is CUDA — the software ecosystem that powers most AI development worldwide.

CUDA has become deeply embedded into:

- machine learning frameworks,

- AI research,

- enterprise infrastructure,

- and developer workflows.

However, competitors are increasingly trying to weaken Nvidia’s software moat. AMD’s ROCm ecosystem, open-source AI tooling, and custom accelerator platforms are all improving rapidly.

CUDA still dominates today, but software ecosystems can eventually shift — especially if customers become desperate to reduce dependence on a single vendor.

Could the AI Boom Become a Bubble?

Another major risk is the possibility of AI overinvestment.

Technology companies are currently spending hundreds of billions of dollars on:

- GPUs,

- AI data centers,

- networking,

- cloud infrastructure,

- and energy expansion.

The assumption is that AI demand will continue growing exponentially for years.

But if:

- enterprise adoption slows,

- AI monetization disappoints,

- or investor enthusiasm weakens,

the industry could face a painful correction similar to previous tech bubbles.

Even Nvidia’s extraordinary growth may eventually normalize.

Antitrust and Regulatory Scrutiny

Nvidia’s dominance is becoming so large that regulators may eventually pay closer attention.

The company now controls critical layers of the AI ecosystem:

- GPUs

- networking

- AI software

- supply chain influence

- data-center infrastructure

Governments in the US, Europe, and China are increasingly concerned about concentrated control over strategic technologies. If Nvidia becomes viewed as too dominant, regulators could eventually impose restrictions or launch antitrust investigations.

Packaging and Manufacturing Bottlenecks

Ironically, Nvidia’s biggest problem may simply be physics and manufacturing capacity.

Advanced AI chips require:

- cutting-edge packaging,

- HBM memory,

- advanced lithography,

- and highly specialized manufacturing processes.

Much of this depends on companies like:

- TSMC

- Samsung

- SK Hynix

Building new semiconductor fabs and advanced packaging facilities can take years. Even unlimited demand cannot instantly create more manufacturing capacity.

For now, demand still vastly exceeds supply. But Nvidia’s future growth may increasingly depend not on innovation alone — but on whether the global semiconductor supply chain can keep up with the AI revolution.

Frequently Asked Questions (FAQ)

Q1: Is Nvidia’s growth sustainable?

A: In the near term, yes. Demand for AI compute far outstrips supply. In the long term, hyperscaler custom chips and neocloud competition will erode Nvidia’s market share, but the company’s software moat (CUDA) provides durable protection.

Q2: Why did Nvidia’s stock drop after record earnings?

A: The stock barely moved (down ~1%). Investors worried about Rubin delays, slower‑than‑expected HBM4 memory speeds, and the fact that Nvidia’s stock is already priced for perfection.

Q3: What is the “Rubin delay”?

A: Nvidia’s next‑gen “Vera Rubin” platform will ship later than originally planned, and the highest‑end Rubin chips have been pushed back several months. However, demand for current‑gen Blackwell chips remains so strong that Nvidia raised its Q2 guidance anyway.

Q4: How does this connect to your article on HBM memory?

A: Directly. HBM is the single biggest bottleneck in Nvidia’s supply chain. Our article “Why HBM Memory Is the New GPU” explained the shortage. Nvidia’s earnings confirm it: every HBM chip is sold out, and Nvidia is forcing Samsung to repurpose lines to meet demand.

Q5: What about competition from Google, Amazon, and Microsoft?

A: Their custom chips are real, but none can match Nvidia’s CUDA software ecosystem or full‑stack integration — yet. Over 3–5 years, they will erode share, but Nvidia will remain dominant.

Q6: Is Nvidia a buy after this earnings report?

A: This article does not provide investment advice. However, the company’s fundamentals are extraordinarily strong, and the capital return program is generous.

Q7: What is SoftBank’s connection to Nvidia?

A: SoftBank owned ARM, which Nvidia tried to buy. After the deal was blocked, SoftBank took ARM public, raising billions. SoftBank is also a major investor in OpenAI and the Stargate AI infrastructure project — all of which benefit from Nvidia’s hardware.

Q8: Where can I learn more about Nvidia’s long‑term strategy?

A: Check out our related articles: “Why Is Nvidia Still Dominating the AI Chip Market? (7 Moat Factors)” and “Why Nvidia Is Investing Billions to Secure Data Center Capacity (IREN Deal Explained).”

Conclusion – The AI Engine Shows No Signs of Slowing

Nvidia’s $81.6 billion quarter is not an outlier — it is the new normal. The company has transformed from a gaming GPU maker into the indispensable infrastructure provider for the entire AI industry.

The muted stock reaction tells us less about Nvidia and more about the surreal expectations it has created. When a company beats estimates by billions, raises its dividend 25‑fold, and announces an $80 billion buyback — and the stock barely moves — that is a sign of success, not failure.

The AI boom is real. And Nvidia is still the engine.

References & Further Reading

- NVIDIA Q1 2026 Earnings Release (May 20, 2026)

- NVIDIA Q1 2026 Earnings Call Transcript (May 21, 2026)

- Bloomberg – “Nvidia’s $81.6B Quarter Shows AI Boom Is Accelerating” (May 21, 2026)

- Reuters – “Nvidia forecasts 91B Q2 revenue, announces 80B buyback” (May 21, 2026)

- CNBC – “Why Nvidia stock barely moved after record earnings” (May 21, 2026)

- The Wall Street Journal – “Nvidia’s Rubin delay raises questions, but demand remains insatiable” (May 21, 2026)

- Financial Times – “SoftBank stock surges 20% on Nvidia earnings, ARM IPO success” (May 21, 2026)

Leave a Reply